Research Article | DOI: https://doi.org/10.31579/2637-8914/205

*Corresponding Author: Samer Younes, Department of Pharmacy, Tartous University, Syria.

Citation: Samer Younes, (2024), The influence of food tax on island places, J. Nutrition and Food Processing, 7(5); DOI:10.31579/2637-8914/205

Copyright: © 2024, Samer Younes. This is an open access article distributed under the Creative Commons Attribution License, which permits unrestricted use, distribution, and reproduction in any medium, provided the original work is properly cited.

Received: 26 March 2024 | Accepted: 19 April 2024 | Published: 01 May 2024

Keywords: food; tax; island

Noncommunicable diseases (NCDs) are the primary cause of premature mortality in Pacific Island Countries and Territories (PICTs), as well as in numerous other jurisdictions worldwide. The Pacific region has declared an NCD crisis and has recommended the implementation of food taxation policies to address the dietary risk factors associated with these diseases. However, the progress in this regard remains uncertain.The review focused on food taxation policies, including excise taxes and tariffs, that were implemented between 2000 and 2020 in 22 PICTs. The key characteristics of these policies were examined. The search for relevant information was conducted using databases, government legal repositories, and broad-based search engines. The identified documents for screening included legislation, reports, academic literature, news articles, and grey literature. Additionally, key informants from each PICT were contacted to gather further data and validate the findings. The results were analyzed through narrative synthesis. Out of the 22 PICTs included in the study, 14 had implemented food taxation policies, and 5 had introduced excise taxes. Processed foods, sugar, and salt were the primary targets of these excise taxes. A total of 84 changes in food taxation policies were identified across all food groups. Among these changes, a total of 279 taxes were identified based on food groups, with 85% being tariffs and 15% being excise taxes. The individual tax rates varied significantly. The most common tax design was ad valorem, followed by volumetric.

Pacific Island Countries and Territories (PICTs) are experiencing some of the highest rates of noncommunicable diseases (NCDs) globally. These include cardiovascular disease, diabetes, cancer, and chronic respiratory diseases, which are prevalent in the region. In fact, up to 90% of deaths in PICTs can be attributed to NCDs. The challenges related to NCDs are similar across the 22 nations in the region, and the rapid changes in dietary habits have contributed to the growth of these diseases.

Many PICTs heavily rely on food imports, which make up a significant portion of their dietary intake. In some PICTs, food imports account for around 40% to 50% of the diet, and in Palau, it exceeds 80% (in the 2000s). However, it is likely that these levels have increased since then. Recognizing the importance of dietary policies in addressing the NCD crisis, PICTs have developed various plans and measures over the past few decades.

One effective fiscal instrument that has been utilized is food taxation policy. Studies have shown that implementing taxes on sugar-sweetened beverages (SSBs) has been widely adopted in PICTs. However, there is currently no systematic identification of food taxation policies and their characteristics in the region. Having an inventory of current taxation policies and their changes over time can provide valuable evidence for policymakers to improve nutrition outcomes and identify opportunities for policy updates.

Furthermore, the use of food taxation policy in PICTs demonstrates their commitment to implementing the recommendations of the World Health Organization (WHO) in addressing NCDs. This showcases the proactive actions taken by these countries, which are classified as low- and middle-income countries (LMICs), in championing public health initiatives.

This fundamental knowledge can provide support for utilizing taxation policy as a means of promoting health and addressing the crisis of non-communicable diseases (NCDs). Furthermore, it can contribute to the existing understanding of food taxes and tariffs within the context of Small Island Developing States. The objective of this research was to conduct a systematic review of food tax policies, specifically examining any tariffs or excise taxes on food that were introduced or modified by Pacific Island Countries and Territories (PICTs) between 2000 and 2020.

The study design involved a systematic search to compile a comprehensive list of enacted taxation policies related to food in PICTs, and to analyze their characteristics. Each individual taxation change served as the unit of analysis.

Inclusion and exclusion criteria

The scope of this study encompassed policies from 22 PICTs (Figure 1), while larger countries in the Pacific region such as New Zealand and Australia were excluded. The focus was specifically on Small Island Developing States. The included taxation policies consisted of excise taxes and tariffs on foods that were implemented between January 2000 and December 2020. Taxes were considered if they were applied to groups of foods or specific food products in a variable manner. These taxes could be imposed on locally produced foods, imported foods, or both, and could be based on factors such as the product's value, volume, or content. This study solely examined taxes implemented at a national level. Taxes that were uniformly applied to all foods at a flat rate were excluded. Additionally, taxation policies that granted tax exemptions to specific regions or industries were also excluded. The analysis did not explicitly consider subsidies.

Both English and French language taxation policies were included in this study, while policies published in Pacific languages were excluded as they were also available in English.

To gather information on taxation policies, four different search approaches were employed. The first approach involved utilizing the Pacific Islands Legal Information Institute (PacLII) database. The second approach consisted of conducting searches on prominent search engines such as Google, Google Scholar, Factiva, and Scopus. For each search engine, the first 50 results were examined. The third approach involved accessing available repositories of government legislation from the Pacific Island Countries and Territories (PICTs). Lastly, key informants were contacted to provide any additional data or advice.

The searches focused on identifying relevant documents, including legislation, government policies, journal articles, grey literature, news articles, and websites that contained information on taxation policies related to foods. The primary type of documentation sought was legislation, specifically Acts. Other forms of documentation were collected to determine the existence of food taxation policies, with an emphasis on locating the corresponding legislation whenever possible. Throughout the search process, a ledger was maintained to record the progress and findings.

The search terms employed varied depending on the search engine or approach being utilized. For instance, when searching the PacLII database for each PICT, specific terms such as "customs duty,""customs levy,""customs tariff,""excise,""excise tax,""import duty,""import levy,""import tariff," and "tariff" were used. Further details regarding the search terms can be found in the Supplementary Material.

To ensure comprehensive data collection, key informants and stakeholders from the PICTs were engaged. Their involvement aimed to gather additional information, address any missing data or inconsistencies, and assess the overall completeness of the data collection process.

To gain a better understanding of the process of extracting data and to distinguish between taxation policies and individual taxes applied to different food groups, refer to Figure 2. Tariffs are measures imposed on imported goods upon their entry into a jurisdiction and do not apply to domestically produced goods. Import duties, excise duties (which only apply to imports), and import levies are all considered tariffs due to their similar nature. Excise taxes, on the other hand, are applied to both domestically produced and imported products.

The analysis conducted involved a directed content analysis of the policies based on specific characteristics of interest. Taxation policies were categorized into excise taxes and tariff policies, and further divided into individual taxes based on food groups. Due to the large number of individual food products mentioned in the documentation, the foods were grouped into nine main categories for reporting purposes. These categories were determined based on the nutrition guidelines developed by the Pacific Community (SPC), which are specifically tailored to a Pacific diet. The nine food groups include: whole grains and carbohydrate-dense vegetables, refined grains and cereals, processed foods, sugar, and salt, fresh and frozen fruits and vegetables, canned fruits and vegetables with low salt or sugar, dried fruits and high-sodium processed vegetables, lean proteins, canned meat and fatty cuts of meat, and processed meats and high-fat dairy and oils. Beverages were excluded from the analysis as they have already been reviewed elsewhere (18).

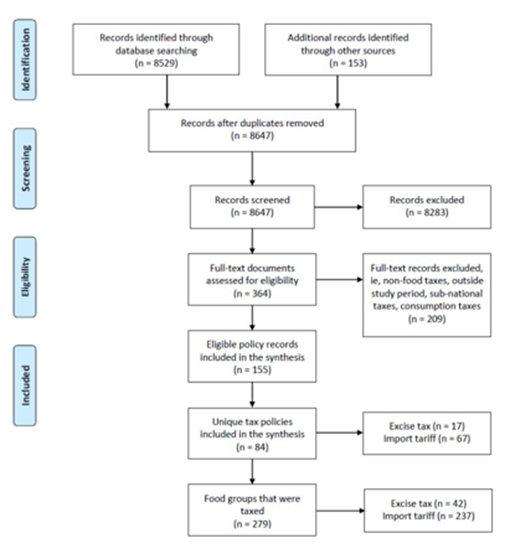

Figure 2. PRISMA Flow Diagram, with the Number of Taxation Policies, Excise Taxes and Tariff Policies, and Individual Taxes

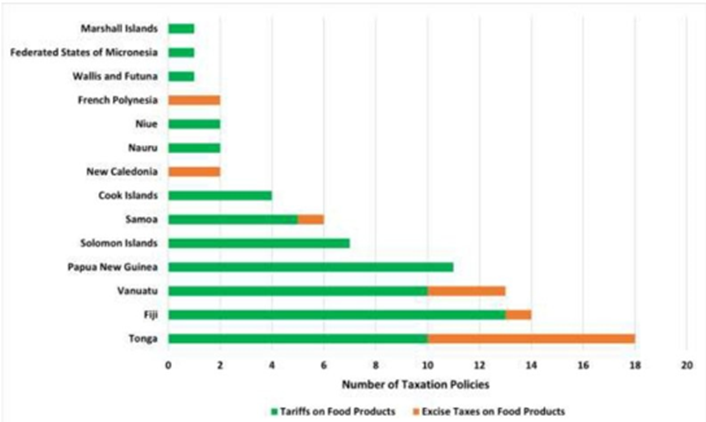

In the search conducted, a total of 8682 documents were chosen for screening. These documents included legislation, reports, academic literature, and news articles. Out of these, 155 information sources met the inclusion criteria of the study and were considered as the data analyzed in the results (Figure 3). Throughout the study period, 14 out of 22 Pacific Island Countries and Territories (PICTs) implemented taxation policies on food that aligned with the study's definition. Additionally, 6 out of 22 PICTs introduced excise taxes specifically on food. Figure 3 illustrates the number of tariffs and excise taxes resulting from the taxation policies, while Figure 4 displays the number of tariffs and excise taxes in each of the 14 PICTs with taxation policies. It is noteworthy that only four PICTs implemented both excise taxes and tariffs, while 12 PICTs solely implemented tariffs and two PICTs solely implemented excise taxes. In cases where both types of taxation policies were present, there were instances where one tax type replaced the other. For example, the implementation of an excise tax led to a reduction in the tariff rate for the same food item. Furthermore, certain tax types were simultaneously applied to food items. At the policy level, a total of 17 excise taxation policies and 67 tariff policies were introduced during the study period, resulting in a combined total of 84 unique food taxation policies. The highest number of new policies implemented in a single year was in 2018, with a total of nine policies. These 84 food taxation policies encompassed a total of 279 tax changes that specifically targeted various food groups. While tariffs were applied to foods from all nine food groups, excise taxes were only applied to food from five of these groups.

Figure 3. Number of food taxation policies in Pacific Island Countries and Territories by tax type (2000-2020)

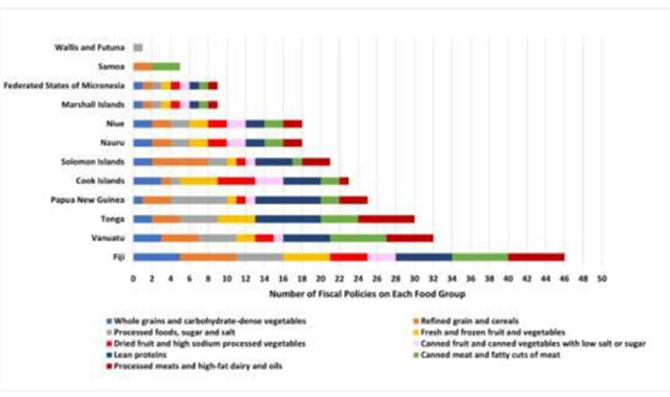

Figure 4. Number of individual tariffs implemented on each food group by Pacific Island Country and Territory (2000-2020)

Figure 5 illustrates the number of tariffs imposed on each food group (n=237) across the 12 PICTs with a tariff policy. In most cases, a single policy encompassed tariffs for the majority, if not all, of the food groups. Tariff taxation policies seemed to be implemented when a PICT aimed to comprehensively update tariff rates or make extensive revisions to the entire tariff schedule. These tariff changes were spread out over the study period. Almost all PICTs experienced at least one tariff change for every food group during this time. Notably, more than half of the import tariffs (138 out of 237, 58%) were applied to less healthy food groups, such as refined grains and cereals, processed foods, sugar and salt, dried fruit and high-sodium processed vegetables, canned meat and fatty cuts of meat, and processed meats and high-fat dairy and oils (Figure 5). This suggests that, on average, tariff changes did not specifically target particular food groups, except for three PICTs that imposed tariffs on specific foods.

Tariff rates varied significantly across the PICTs, ranging from 0% to 300

During the study period, there was an increase in the number of excise taxes imposed on food. The earliest introduction of excise taxes was observed in French Polynesia in 2001, with subsequent changes in 2019. On the other hand, Vanuatu implemented excise taxes more recently in 2010, 2012, and 2014, followed by Tonga from 2013 to 2018, Samoa in 2016, and New Caledonia in 2018 and 2019 [16].

Unlike tariffs, most of the identified food excise taxes in this study were newly implemented taxes rather than changes in tax rates. In one instance, Fiji reversed excise taxes by removing sugar from the Excise Tax Act Schedule. Similar to tariffs, there was significant variation in the excise tax rates, even within different food groups[5]. Provides an overview of the upper and lower excise tax rates for each Pacific Island Country and Territory (PICT) from 2000 to 2020, categorized by food group. The introduced excise taxes ranged from up to 8% in Samoa to 22% in New Caledonia, and up to TOP 5/kg in Tonga (equivalent to US$2.10), CFP 120/kg in French Polynesia (equivalent to US$1.10), and VT 20/kg in Vanuatu (equivalent to US$0.17). Most excise tax designs followed a volumetric approach, although some utilized ad valorem and tiered tax designs. For instance, French Polynesia implemented a tiered volumetric tax based on the sugar content or volume of sugar in various food products such as biscuits, ice cream, jams, and chocolate[7,26].

Out of the nine food groups examined, five were specifically targeted for tariff and excise policies. These groups included refined grains and cereals, processed meats and high-fat dairy and oils, lean proteins, canned meat and fatty cuts of meat, and processed foods, sugar, and salt. The taxed products within these groups often aligned with the recommendations of the Secretariat of the Pacific Community (SPC) to consume less or limit their intake. Notably, none of the excise taxes were applied to products within the fruit and vegetable food groups, and tariffs were also less common in this category.

The findings derived from this study reinforce and expand upon existing research by providing a comprehensive overview of food-specific taxation policies in the Pacific Island Countries and Territories (PICTs) during the review period. Additionally, this study presents novel information that has not been previously reported in other studies on food taxation policies in the Pacific region.

One of the strengths of this study is its ability to provide detailed insights into the characteristics of food taxation policies within the PICTs. This includes information on the specific types of foods and food groups that are subject to taxes, as well as the jurisdictions in which these taxes are implemented. Furthermore, the study sheds light on important aspects of the excise taxes and tariffs, such as their rates and design[19-35].

It is important to note that the majority of the data for this study was obtained from databases and online publications. However, due to potential resource limitations in the small Pacific jurisdictions, these databases may not have been regularly updated, resulting in some gaps in the data. Nevertheless, the study mitigated this issue by triangulating the data from multiple sources, thereby enhancing the validity of the findings.

Future research could delve into the impacts of food taxes in the Pacific region and explore the factors that facilitated their implementation, drawing upon previous studies that have evaluated the effects of food taxes. It is worth mentioning that the study was unable to explicitly examine the rationale behind tax changes, as this information was not consistently available from legislation and other collected data. However, in certain cases, this information may be accessible through alternative sources[31-34].

In terms of implications, the study recommends the application of excise taxes on both imported products and domestically produced goods as a means of preventing non-communicable diseases (NCDs). Maintaining consistency in the excise tax rates between imported and domestically produced foods can help reduce the substitution of equally unhealthy domestically produced products. Furthermore, excise taxes are less susceptible to changes necessitated by trade agreements, such as the removal of the turkey tail ban in Samoa and subsequent reduction in tariffs[36-38].

Hence, implementing comprehensive and effective policies such as excise taxes can be more advantageous than tariffs in reducing the consumption of specific foods. This approach holds potential for expansion in the Pacific region and other areas to further promote health objectives. However, the success of excise taxes in improving health outcomes and reducing non-communicable diseases (NCDs) while minimizing negative externalities depends on their design. In the Pacific Island Countries and Territories (PICTs), excise taxes will be most impactful when applied to foods that are recognized as major contributors to NCDs in these regions. To achieve this, utilizing a Pacific-oriented nutrient profiling tool to systematically identify food products suitable for excise taxation could prove to be an effective strategy. It is preferable for excise taxes to be nutrient-specific, targeting the sugar, salt, or fat content of products, rather than being ad valorem (based on product value) or volumetric (based on product volume or weight). Nutrient-specific tax designs have shown to be more effective in reducing the quantity of unhealthy components in food products, thereby reducing their consumption[39,40]. Additionally, they help alleviate the tax burden on populations, particularly lower-income groups, thus promoting equity. Volumetric taxes on food also have advantages over ad valorem taxes as they have a greater impact on reducing bodyweight and can potentially avoid regressive tax burdens. However, it is important to regularly adjust nutrient and volumetric taxes to account for inflation and maintain their real value and effectiveness. Implementing such taxes may pose challenges but can be crucial in achieving desired health outcomes. When considering the taxation of any food group, it is essential to assess the equity impacts, particularly when viable alternatives are limited. For instance, taxing certain meat products may negatively affect equity if these products serve as key protein sources for specific populations[35,40-42].

Combined policies that implement higher taxes on less healthy food and lower taxes on healthy food have the potential to encourage individuals to make healthier food choices and promote fairness in society. Additionally, allocating the tax revenue towards increased spending on healthcare can further enhance equity. In the Pacific region, food taxes have been utilized to achieve various policy objectives. Between 2000 and 2020, a significant number of Pacific Island Countries and Territories (PICTs) have implemented excise taxes specifically targeting unhealthy foods, which have shown promising results in improving health outcomes. There is an opportunity to further strengthen food taxation policies in response to the non-communicable disease (NCD) crisis in the Pacific. This can include the wider adoption of tiered or nutrient-specific excise taxes that are consistently applied to unhealthy food items.

Dear Editorial Team, Clinical Medical Reviews and Reports. My experience with the journal was highly positive. The peer-review process was rigorous, constructive, and completed in a timely manner. The reviewers provided valuable comments that helped improve the quality and clarity of our manuscript. The editorial office was professional, responsive, and supportive throughout all stages of the publication process. Communication was clear and efficient, and any questions were addressed promptly. Overall, I found the journal to maintain high scientific standards and an excellent publication workflow. I would be pleased to consider submitting future work to this journal. Best wishes from, Elena Popa.

It was my pleasure to submit my testimonial concerning the Reviewer Board of our Scientific Journal “Brain and Neurological Disorders”. The Reviewers focused on some modifications and their contribution was helpful. The ladies of our Editorial Office were also supported my efforts. It was my honor to have such a co-operation and I am looking forward for more collaboration.

Dear Grace Pierce, Editorial Coordinator of Journal of Clinical Research and Reports, Thank you for the speedy and efficient peer review process. I appreciate the fact that your peer reviewers do not take months to respond like with some other journals. I would also like to thank the editorial office for responding quickly to my questions. It is an excellent journal. I plan to submit more manuscripts in the future. Best wishes from, Robert W. McGee

Dear Grace Pierce, Editorial Coordinator of Journal of Clinical Research and Reports, Working with you and your team on our recent publication in JCRR has been a truly wonderful and enjoyable experience. The responses were prompt, and the reviewers were patient, constructive, and highly professional. One reviewer in particular gave me the feeling that a professor was carefully reading and commenting on my coursework, which was deeply touching. The entire process was straightforward and hassle‑free, with no tedious online forms to complete. I highly recommend this journal. Best wishes from, DR Aibing Rao, Head of R&D

I Appreciate the Opportunity to Share my Experience with the Journal of Clinical Research and Reports. The peer review process was timely and constructive, and the feedback provided helped improve the quality of our manuscript. The editorial office was professional, responsive, and supportive throughout the process, ensuring smooth communication and efficient handling of the submission. Overall, it was a positive experience collaborating with your team.

Dear Mercy Grace, Editorial Coordinator of Obstetrics Gynecology and Reproductive Sciences, We would like to express our gratitude for your help at all stages of publishing and editing the article. The editors of the magazine answer all the necessary questions and help at every stage. We will definitely continue to cooperate and publish other works in the Obstetrics Gynecology and Reproductive Sciences! Best wishes from, Alla Konstantinovna Politova,